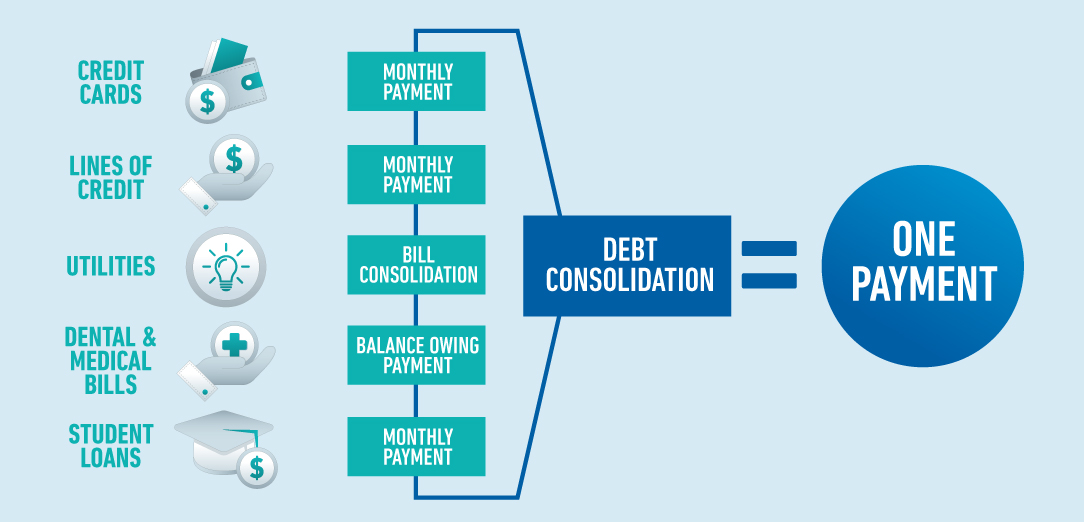

Debt consolidation rolls multiple debts into a single payment. It can be a good idea if you qualify for a low enough interest rate.

Many or all of the products featured here are from our partners who compensate us. This influences which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here’s how we make money.

Debt consolidation rolls multiple debts, typically high-interest debt such as credit card bills, into a single payment. Debt consolidation might be a good idea for you if you can get a lower interest rate than you’re currently paying. That will help you reduce your total debt and reorganize it so you can pay it off faster.

If you’re dealing with a manageable amount of debt and just want to reorganize multiple bills with different interest rates, payments and due dates, debt consolidation is a sound approach you can tackle on your own.

Nerdy Takeaways

Two ways to consolidate debt are by getting a balance-transfer credit card with a 0% APR introductory period, or by getting a fixed-rate debt consolidation loan.

Debt consolidation is a good idea if your monthly debt payments (including mortgage or rent) don’t exceed 50% of your monthly gross income, and if you have enough cash flow to cover debt payments.

Debt consolidation isn’t a quick fix for severe debt problems.

How to consolidate your debt

There are two primary ways to consolidate debt, both of which concentrate your debt payments into one monthly bill. The best option for you will depend on your credit score and profile, as well as your debt-to-income ratio.

Get a 0% interest, balance-transfer credit card: Transfer debt onto this card and then be sure to pay it off during the promotional period to get the interest-rate break. You will likely need good or excellent credit (690 or higher) to qualify.

Get a fixed-rate debt consolidation loan: Use the money from the loan to pay off your debt, then pay back the loan in installments over a set term. You can qualify for a loan if you have bad or fair credit (689 or below), but borrowers with higher scores will likely qualify for the lowest interest rates.

Two additional ways to consolidate debt are taking out a home equity loan or borrowing from your retirement savings with a 401(k) loan. However, these two options involve risk — to your home or your retirement.

Debt consolidation calculator

Use the calculator below to see whether or not it makes sense for you to consolidate.

When debt consolidation is a smart move

Success with a consolidation strategy requires the following:

Your monthly debt payments (including your rent or mortgage) don’t exceed 50% of your monthly gross income.

Your credit is good enough to qualify for a credit card with a 0% interest period or low-interest debt consolidation loan.

Your cash flow consistently covers payments toward your debt.

If you choose a consolidation loan, you can pay it off within five years.

Here’s an example when consolidation makes sense: Say you have two or three credit cards with interest rates ranging from 11.21% to 25.7%, and your credit is good. You might qualify for an unsecured debt consolidation loan at 7.99% — a significantly lower interest rate. With less interest accruing each month, you’ll make quicker progress toward being debt-free.

For many people, consolidation reveals a light at the end of the tunnel. If you take a loan with a three-year term, you know it will be paid off in three years — assuming you make your payments on time and manage your spending. Conversely, making minimum payments on credit cards could mean months or years before they’re paid off, all while accruing more interest than the initial principal.

Is it a good idea to consolidate credit cards?

Consolidate your debt if you can get a better interest rate and/or it will help you make payments on time. Just make sure this consolidation is part of a larger plan to get out of debt and you don’t run up new balances on the cards you’ve consolidated. Read about how to tackle credit card debt.

How does a debt consolidation loan work?

A personal loan allows you to pay off your creditors yourself, or you can use a lender that sends money straight to your creditors. Read about the steps required to get a personal loan.

Do debt consolidation loans hurt your credit?

Debt consolidation can help your credit if you make on-time payments or if consolidating shrinks your credit card balances. Your credit may be hurt if you run up credit card balances again, close most or all of your remaining cards, or miss a payment on your debt consolidation loan. Learn more about how debt consolidation affects your credit score.

When debt consolidation isn’t worth it

Consolidation isn’t a cure-all for all of your debt problems. You will still need to take steps such as seeking low-cost financial advice or lowering your living expenses. It’s also not the solution if you’re overwhelmed by debt and have no hope of paying it off even with reduced payments.

If your debt load is small — you can pay it off within six months to a year at your current pace — and you’d save only a negligible amount by consolidating, don’t bother. Instead, try a do-it-yourself debt payoff method instead, such as the debt snowball or debt avalanche. You can use a credit card payoff calculator to test out the different strategies.

If the total of your debts is more than half your income, and the calculator above reveals that debt consolidation is not your best option, you’re better off seeking debt relief than treading water.